- Do all cryptocurrencies use blockchain

- Are all cryptocurrencies based on blockchain

- Market cap of all cryptocurrencies

Are all cryptocurrencies based on blockchain

In conclusion, not all cryptocurrencies are mined. While mining remains a popular method for creating digital currencies, especially through PoW consensus mechanisms, other cryptocurrencies are generated through staking, pre-mining, or airdrops https://drying-machine.org/. Each method has its advantages, depending on the goals of the project, whether that’s decentralization, energy efficiency, or network stability. As I continue to explore the ever-evolving world of cryptocurrencies, it’s clear that there are many paths to creating a digital currency, and mining is just one of them.

How you mine a particular cryptocurrency varies slightly depending on the type of cryptocurrency being mined, but the basics are still the same: mining creates a system to build trust between parties without needing a single authority and ensures that everyone’s cryptocurrency balances are up-to-date and correct in the blockchain ledger.

Sometimes, two miners broadcast a valid block at the same time, and the network ends up with two competing blocks. The miners then start mining the next block based on the block they received first, causing the network to split into two different versions of the blockchain temporarily.

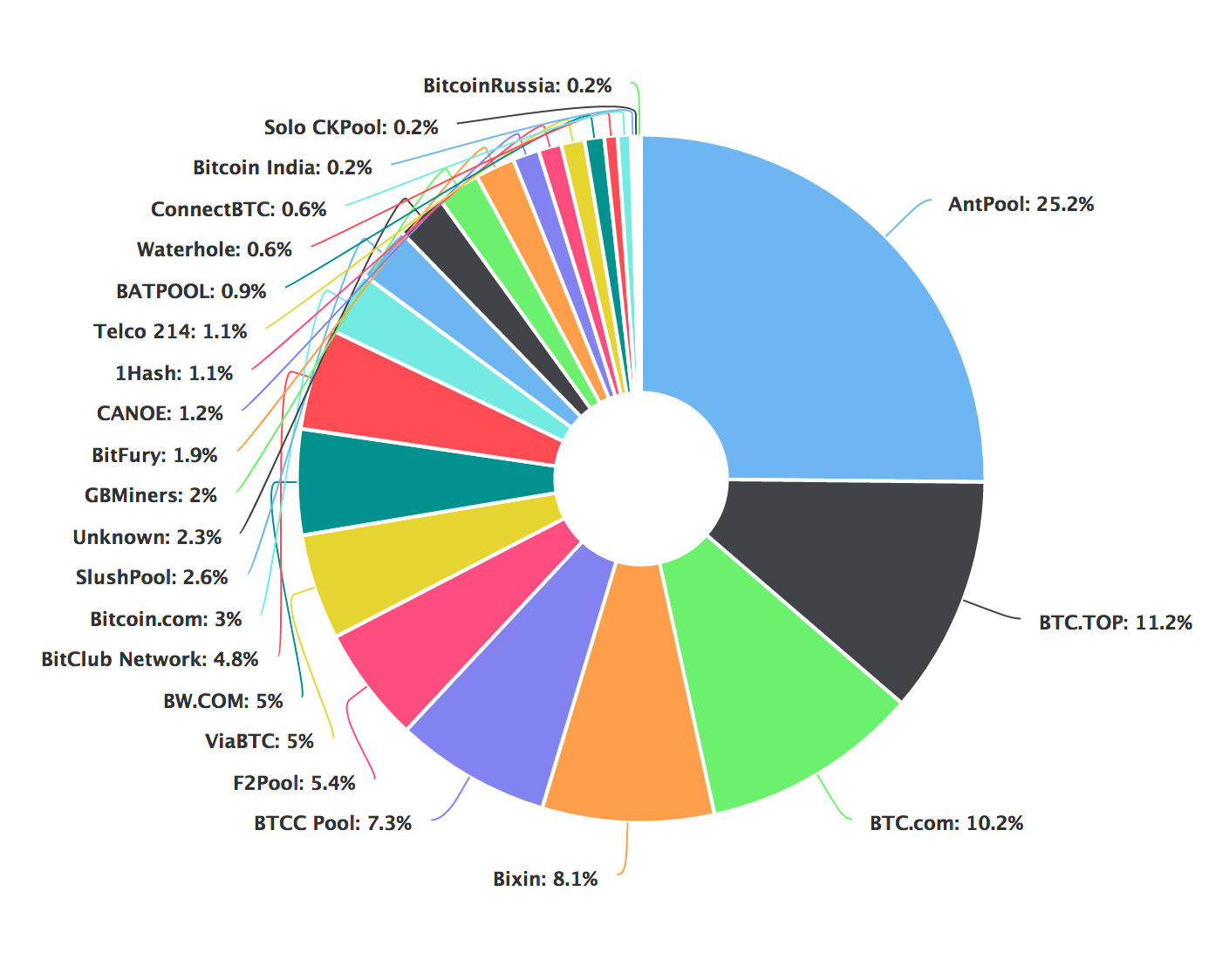

Every time new miners join the network and competition grows, the hashing difficulty increases, which prevents the average block time from decreasing. Conversely, if many miners leave the network, the hashing difficulty decreases, making it easier to mine a new block. These adjustments keep the average block time constant, regardless of the network’s total hashing power.

Do all cryptocurrencies use blockchain

One of the best blockchain platforms, Ethereum, was released in 2013. It offers a blockchain that is as fully decentralized as the Bitcoin blockchain network. Ethereum is also completely decentralized and boasts complete support for smart contracts.

A blockchain consists of programs called scripts that conduct the tasks you usually would in a database: entering and accessing information, and saving and storing it somewhere. A blockchain is distributed, which means multiple copies are saved on many machines, and they must all match for it to be valid.

Using blockchain in this way would make votes nearly impossible to tamper with. The blockchain protocol would also maintain transparency in the electoral process, reducing the personnel needed to conduct an election and providing officials with nearly instant results. This would eliminate the need for recounts or any real concern that fraud might threaten the election.

According to the definition of cryptocurrency, the answer is no. The defining characteristic of any cryptocurrency is that security is ensured with cryptography. Moreover, cryptocurrencies aren’t issued by a central authority, like a bank. In theory, this makes them immune to government interference or manipulation.

Because of the decentralized nature of the Bitcoin blockchain, all transactions can be transparently viewed by downloading and inspecting them or by using blockchain explorers that allow anyone to see transactions occurring live. Each node has its own copy of the chain that gets updated as fresh blocks are confirmed and added. This means that if you wanted to, you could track a bitcoin wherever it goes.

Are all cryptocurrencies based on blockchain

Cryptocurrency and blockchain are two distinct technologies that complement each other. The blockchain serves as the underlying technology that supports the cryptocurrency network, recording all transactions and creating new blocks to record successful ones.

Healthcare providers can leverage blockchain to store their patients’ medical records securely. When a medical record is generated and signed, it can be written into the blockchain, which provides patients with proof and confidence that the record cannot be changed. These personal health records could be encoded and stored on the blockchain with a private key so that they are only accessible to specific individuals, thereby ensuring privacy.

This could become significantly more expensive in terms of both money and physical space needed, as the Bitcoin blockchain itself was over 600 gigabytes as of September 15th, 2024—and this blockchain records only bitcoin transactions. This is small compared to the amount of data stored in large data centers, but a growing number of blockchains will only add to the amount of storage already required for the digital world.

The settlement and clearing process for stock traders can take up to three days (or longer if trading internationally), meaning that the money and shares are frozen for that period. Blockchain can, in theory, drastically reduce that time.

Cryptocurrency and blockchain are two distinct technologies that complement each other. The blockchain serves as the underlying technology that supports the cryptocurrency network, recording all transactions and creating new blocks to record successful ones.

Healthcare providers can leverage blockchain to store their patients’ medical records securely. When a medical record is generated and signed, it can be written into the blockchain, which provides patients with proof and confidence that the record cannot be changed. These personal health records could be encoded and stored on the blockchain with a private key so that they are only accessible to specific individuals, thereby ensuring privacy.

Market cap of all cryptocurrencies

These crypto coins have their own blockchains which use proof of work mining or proof of stake in some form. They are listed with the largest coin by market capitalization first and then in descending order. To reorder the list, just click on one of the column headers, for example, 7d, and the list will be reordered to show the highest or lowest coins first.

CoinMarketCap does not offer financial or investment advice about which cryptocurrency, token or asset does or does not make a good investment, nor do we offer advice about the timing of purchases or sales. We are strictly a data company. Please remember that the prices, yields and values of financial assets change. This means that any capital you may invest is at risk. We recommend seeking the advice of a professional investment advisor for guidance related to your personal circumstances.

A blockchain is a type of distributed ledger that is useful for recording the transactions and balances of different participants. All transactions are stored in blocks, which are generated periodically and linked together with cryptographic methods. Once a block is added to the blockchain, data contained within it cannot be changed, unless all subsequent blocks are changed as well.

With a blockchain, it’s possible for participants from across the world to verify and agree on the current state of the ledger. Blockchain was invented by Satoshi Nakamoto for the purposes of Bitcoin. Other developers have expanded upon Satoshi Nakamoto’s idea and created new types of blockchains – in fact, blockchains also have several uses outside of cryptocurrencies.

Tokens, on the other hand, are crypto assets that have been issued on top of other blockchain networks. The most popular platform for issuing tokens is Ethereum, and examples of Ethereum-based tokens are MKR, UNI and YFI. Even though you can freely transact with these tokens, you cannot use them to pay Ethereum transaction fees.

Leave a Reply